The coronavirus crisis has triggered unprecedented shockwaves in our societies, with political and business leaders worldwide deciding how to restart economies.

One area of focus is lowering greenhouse gas emissions (GHG) by investing in technologies focused on long-term systemic solutions. Hydrogen is ideally suited to this restart, and can play a significant role at places where direct electrifications fail to excel.

Read more: Coronavirus stimulus spending creates golden opportunity for low-carbon transition

Hydrogen technologies can make our economies cleaner, more secure, and more sustainable by:

• providing zero-emission fuels for long-haul transport and mining

• providing feedstock for significant reductions in GHG emissions in heavy industry

• adding flexibility and system security services to electricity grids

• replacing natural gas in domestic gas networks.

The national and state hydrogen strategies

Australia has abundant wind and solar resources to provide large quantities of cost-competitive green hydrogen – not only for reducing GHG emissions in its own economy, but also for export.

Japan, South Korea, Singapore and Germany are prime markets for Australia to export low-emissions hydrogen or products such as ammonia.

Read more: A breakthrough in green production and storage of hydrogen gas

In November 2019, the Australian federal government launched the National Hydrogen Strategy, aiming to position Australia as a major player in the global hydrogen market by 2030. State governments have embraced this vision, and announced their goals and actions accordingly to support the rollout of a major hydrogen industry.

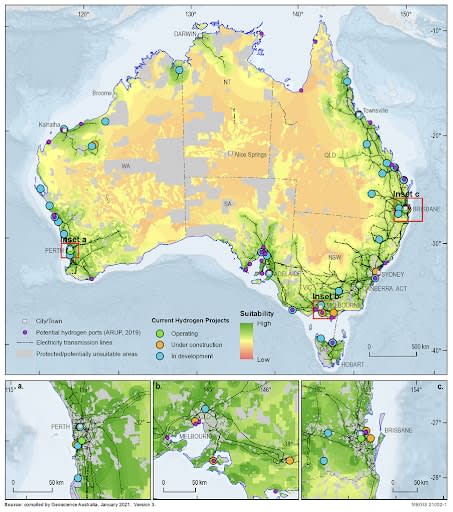

The current demonstration projects

While large-scale hydrogen production has not yet been implemented in Australia, there’s an increasing number of pilot, demonstration and small-scale projects in various development stages, as shown in the map below.

Identifying the economic fairways for hydrogen

To support the implementation of the national and state hydrogen strategies, Geoscience Australia, in collaboration with Monash University, developed an open-source economic model, the Hydrogen Economic Fairways Tool (HEFT), to assess the economic viability of potential hydrogen operations across Australia.

HEFT is a free online tool with the ability to conduct a detailed geospatial-financial analysis of future large-scale hydrogen projects. It not only assesses the quality of energy resources (wind, solar PV, concentrated solar power, steam methane reformation (SMR) with carbon capture and storage (CCS), and coal gasification with CCS) required to produce low-emissions hydrogen, but also considers the associated rail and road transportation infrastructures, pipelines to export ports, and ready access to water, among other factors.

The tool, therefore, could support decision-making by policymakers and investors on the location of new infrastructure and development of hydrogen hubs in Australia.

Read more: Renewables can still play an important role in Australia's energy roadmap

The government’s ‘H2 under $2’ goal could be achieved sooner

The Australian government has set a stretch goal of “H2 under $2” – production of hydrogen for less than A$2 per kg. The speed of achieving this goal depends on many factors, including the momentum of technology adoption, cost reductions, configurations of the hydrogen supply chain, and delivery of supporting infrastructure.

The cost of renewable hydrogen production is a function of electrolyser (for example, proton exchange membrane (PEM), or alkaline) capital investments, costs of renewable generation facilities, and the utilisation factor of the hydrogen plant (that is, up-time per year).

Under assumptions of significant technology cost reduction provided by Bloomberg Energy Futures and renewable deployment in 2030, the HEFT model calculates off-grid hydrogen production costs to be as low as $2/kg, given an optimal mix of wind and solar PV to maximise the utilisation rate of water electrolysis. Adding water and delivery costs would lead to a hydrogen cost just below $3/kg before shipping.

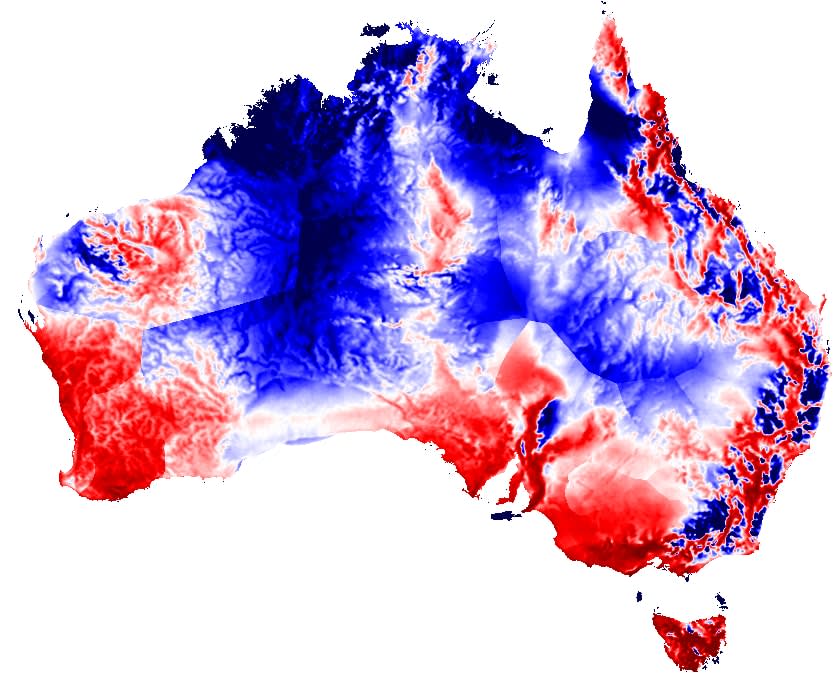

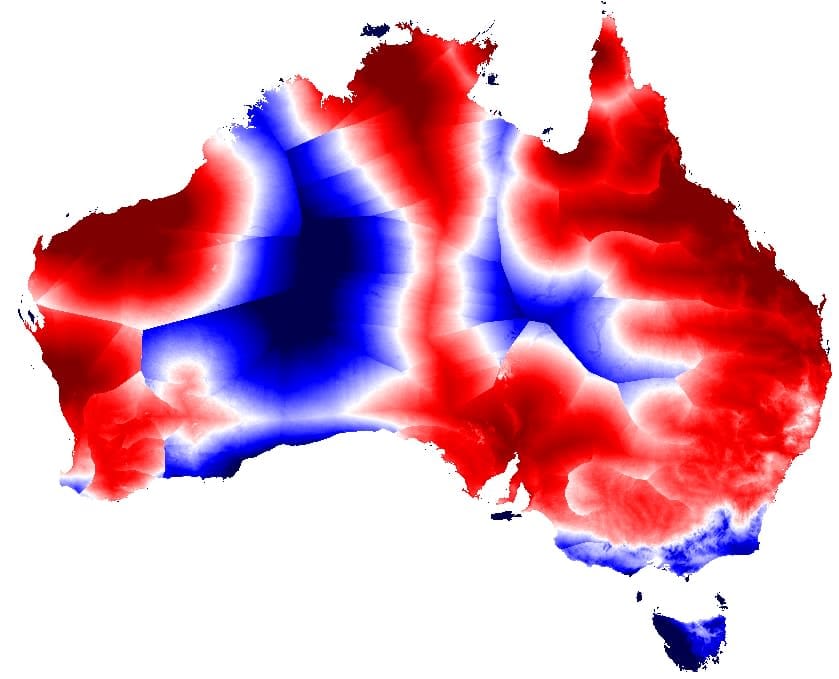

The following sample output from HEFT shows the favourable locations (in red) of potential hydrogen hubs in 2030, with targeted hydrogen market prices of $4.5/kg and $3/kg (including delivery costs) by wind and solar PV, respectively.

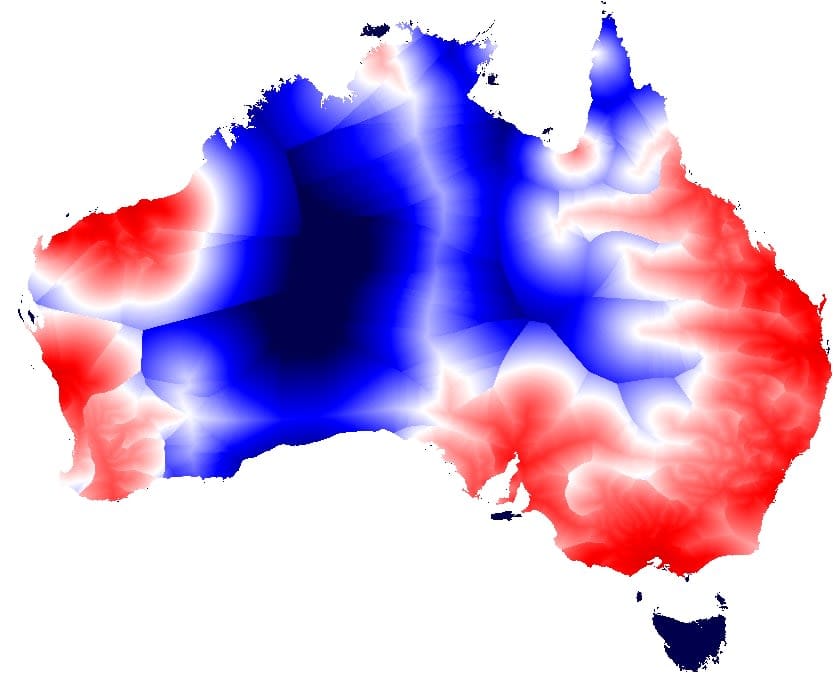

The third graph shows favourable locations of SMR with CCS at a targeted market price of $3.5/kg and a gas price of $7/GJ. The calculations have taken into account future cost projections of hydrogen production plants, renewable electricity generation facilities, fuel, CCS facilities, water, transportation, pipelines to the closest port, and corporate taxes.

Next steps

Geoscience Australia and Monash University are actively expanding the Hydrogen Economics Fairways tool. The ultimate goal is to optimise the development of shared infrastructure to facilitate large-scale hydrogen production and delivery, attracting investment into Australia’s hydrogen industry.

Further inclusions of battery, hydro, pumped hydro energy storage, and delivery infrastructures will be added to the tool.

Large-scale hydrogen storage will also be incorporated in future works. (In a parallel project with Woodside Energy, grid-connected hydrogen production within the national electricity market is also being developed. This addition considers time-dependent electricity wholesale prices and proximity to existing transmission lines.)

The paper is available on EarthArxiv.

This article was co-authored with Laura Easton and Andrew Feitz from Geoscience Australia.